The simple fact is that housing is the most expensive of all human needs; and like any business, without government intervention, housing production by the private sector will always be geared towards effective demand. By effective demand, we mean those with the ability to pay.

Because of this fact, millions of Filipinos are without homes they can call their very own; and all talk of resolving the ever-worsening housing problem would be meaningless without fully addressing one of two primordial issues impinging upon housing development – inadequate homebuyer financing.

Thus, ever since its establishment in 1973, the installation of an effective homebuyer financing system has been at the core of CREBA’s advocacies.

CREBA’s first major success in this regard was the government’s adoption of its recommendation to institute a housing finance infrastructure similar to the US home mortgage system, which has been the US government’s potent tool in encouraging the flow of private capital into housing.

The Rudiments

CREBA’s advocacy resulted in the creation of the National Home Mortgage Finance Corporation (NHMFC) in 1977 – a rudimentary secondary market system for home mortgages, followed by the creation of the Pag-IBIG Fund in 1978 – a mutual fund comprised of mandatory contributions by employers and employees. The Home Development Mutual Fund (HDMF) administered the Pag-IBIG Fund, which was intended to generate funds for home lending purposes. These corporations were attached to the then Ministry of Human Settlements.

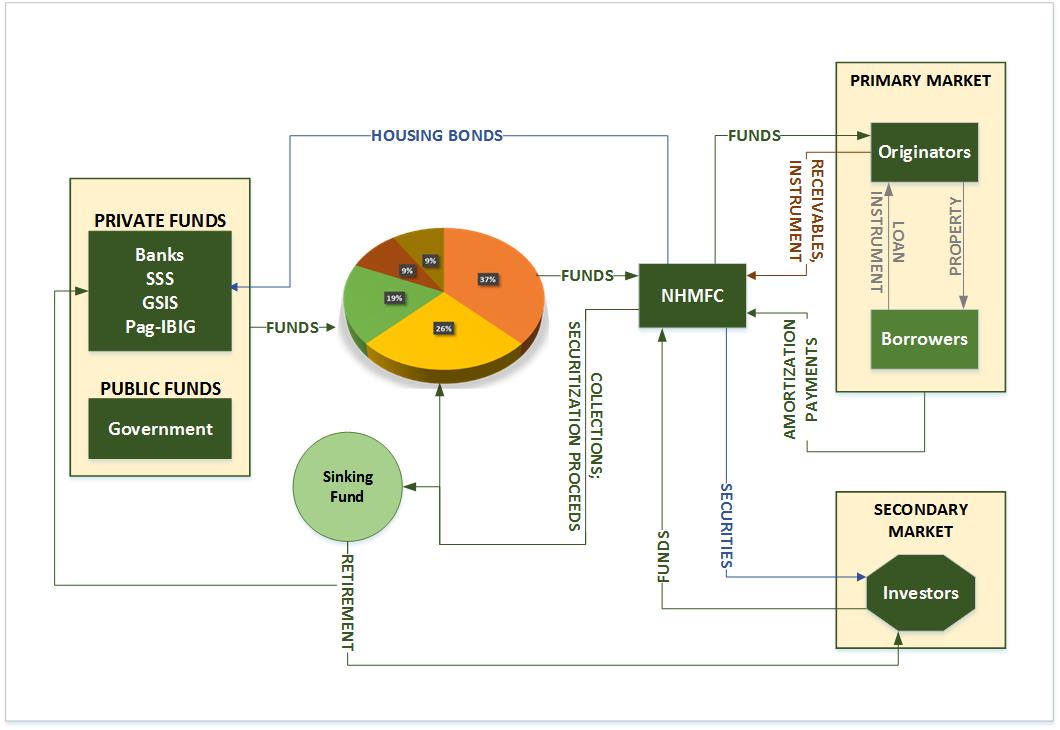

Figure 1 capsulizes the operational concept of this finance infrastructure. When the NHMFC “buys” the mortgages from Pag-IBIG, the receivables therefrom together with the real estate collateral backing them would then represent NHMFC’s assets which it can utilize for “securitization” – i.e. the issuance and trading of its securities in the secondary market.

System for Home Mortgages

Securitization would enable the NHMFC to generate more funds by attracting investments from private institutions through the sale mortgaged-backed instruments, and recycle these funds by purchasing more home mortgages.

With the twin pillars of housing finance in place and offering mortgage take-outs, housing production rose to unprecedented levels.

Nonetheless, CREBA continued to propose reforms to ensure the long-term viability and effectiveness of the fledgling housing finance infrastructure.

This was when the Chamber first advocated its concept of a centralized fund pool – i.e. combining all funds available for housing credit under the disposition of a single shelter finance body. The goals were:

- To allow for more effective and long-term fund programming in accordance with housing production targets and operational thrusts, as well as greater operational control and efficiency;

- To enable the finance system to be self-sustaining on a long-term basis through the revolving of a single large fund pool in secondary mortgage market operations;

- Through centralized lending, to standardize lending terms, procedures, requirements and documentation, thereby improving efficiency and minimizing costs on the part of both developers and homebuyers;

- To allow for the integration of the informal sector (e.g. self-employed) into the mainstream of the economy, thereby providing the opportunity for government to improve tax collection, while enabling them to also enjoy the benefits of the housing finance system; and

- Preclude the need for governmental budgetary support in providing financing assistance to socialized and low-income homebuyers, by enabling a cross-subsidy mechanism where social housing beneficiaries, whether members or non-members of SSS/GSIS/Pag-IBIG, can enjoy affordable loan rates of as low as 9% per annum.

However, as the instability of the Martial Law regime worsened, the economy nose-dived, and a financial meltdown ensued with market interest rates soaring to as high as 80%.

With limited funds and its lending rates pegged at only 9%, NHMFC’s operations became nonviable. Many developers either went bankrupt or lost billions in completed projects that were stuck in the mortgage take-out pipeline.

Under the Cory Aquino Administration

When then President Corazon Aquino came to power in the aftermath of the EDSA Revolution, among her first acts was Executive Order No. 90 which dismantled the MHS machinery and emasculated the Pag-IBIG Fund by abrogating its mandatory character.

CREBA lodged a protest but was ignored by an administration who did “not welcome unsolicited advice.” It was only later – when the Pag-IBIG Fund was drying up and cheap housing loans became unavailable – that employee groups themselves, led by teachers, publicly clamored for the restoration of Pag-IBIG. Consequently, in 1993 – through the efforts of Congressman Amado Bagatsing, a former CREBA President, RA 7742 was enacted to restore the mandatory character of the Fund.

Under EO 90, the Unified Home Lending Program (UHLP) was established. EO 90 also created the Housing and Urban Development Coordinating Council (HUDCC) which was tasked to provide policy directions and guidelines for the operation of the shelter agencies.

The UHLP adopted the centralized fund pool advocated by CREBA. The UHLP Fund – composed of funding commitments out of the investible funds of the SSS, GSIS and Pag-IBIG – was established.

However, departing from the original concept, EO 90 tasked the NHMFC with administering both the secondary AND the primary market for home loans.

The “unified” lending aspect entailed the establishment of a nationwide network of NHMFC-accredited “originators” composed of banks and developers which granted home loans to eligible borrowers, secured by a mortgage on the house/lot packages being bought. The idea was for the originators to grant loans on the strength of the NHMFC’s commitment to purchase the mortgages from the originators, using the UHLP funds. The originators then served as NHMFC’s collecting agents – i.e. collect the amortizations from the borrowers and remit the collections to NHMFC.

CREBA pointed out that the lending aspect was fraught with operational defects, which would result in very poor collection performance and inevitably lead to insolvency and collapse of any funding agency.

Furthermore, the funding commitments were being remitted to the NHMFC in the form of meager loan trickles, fraught with less than reasonable conditionalities. This resulted in:

- Very limited production averaging only some 70,000 units per year;

- Failure to service the greater bulk of the underprivileged particularly those in the informal sector, since the Funders required of NHMFC that only their members shall be entitled to financing assistance under the UHLP; and

- Inability of the NHMFC to embark on securitization, since the funds were infused as “loans” which remained as assets of the Funders, rather than as “investments” which the NHMFC can use as assets to back the issuance and trading of its securities necessary for revolving and generating more funds.

During the consultations on the Urban Development and Housing bill filed by then Senator Jose Lina, CREBA recommended the inclusion of several funding sources for the national shelter program, namely:

- 50% from the annual net income of the Public Estate Authority

- Proceeds from the disposition of ill-gotten wealth

- Flotation of bonds

- Proceeds from the sale or disposition of alienable public lands in urban areas

- 25% of the proceeds from the documentary stamp tax

- 50% of the government’s share in the annual gross eamings of the Philippine Amusement and Gaming Corporation (PAGCOR)

- 20% of the mandatory annual contributions by Philippine Charity Sweepstakes Office (PCSO) to the charity fund

- All unused portions of the annual agri-agra allocation of banks

- 25% of the net proceeds of any sale of portions of military camps

- Proceeds from forfeited customs bonds

- Additional budgetary allocations for NHMFC and NHA.

Of those fund sources, only the first four were included in RA 7279 (UDHA) enacted in 1992. However, in 1994 under the Ramos administration, again through the efforts of Congressman Bagatsing and the supportive House Speaker Jose De Venecis, RA 7835 otherwise known as the Comprehensive and Integrated Shelter Finance Act (CISFA) was enacted, incorporating all the fund sources as proposed by CREBA.

The CISFA also increased NHMFC’s capitalization from P500 Million to P5.5 Billion, and provided and an additional annual allocation of P500 Million as liquidity and interest/subsidy support to NHMFC’s secondary market operations.

Notwithstanding, as predicted by CREBA, the NHMFC continued to suffer liquidity problems.

Under the Ramos Administration

In 1995, the NHMFC sought to remedy its financial difficulties through a drastic policy shift, which was purportedly intended to (1) improve the quality of mortgages purchased by the NHMFC and thus upgrade collection performance, (2) ensure high marketability of mortgages in the SMMS, and (3) assure continued cash flow for the NHMFC.

Under the new paradigm, only employees were to be eligible, a new window for market-oriented loans was to be installed, and loan origination was to be undertaken exclusively by financial institutions (i.e. no origination by developers).

CREBA opposed the measures, contending that those will not solve NHMF’s problems but worse, will negate the purpose for establishing the UHLP.

The CREBA position paper stated:

CREBA fully subscribes to the proposition that (1) the continuing viability of the NHMFC and the SMMS must be preserved and enhanced, and (2) for this purpose, the integrity of home mortgages is indispensable.

It should be emphasized, however, that the UHLP was instituted primarily as a socially oriented program – intended to lower the cost of home financing assistance and facilitate availment thereof by the low-income and underprivileged sectors, which cannot avail of the credit facilities of financing institutions due to high financing costs as well as various stringent and tedious lending prerequisites.

The revisions to the UHLP will serve to negate the very purpose for its establishment, in view of the following adverse impact:

- Those who belong to the informal sector will be effectively denied access to the UHLP since they cannot possibly comply with the documentary requirements under the new set-up.

- The requirement for credit investigation (presumably to be undertaken by banks) will not only entail additional costs which will eventually be passed on to the borrower, but would also result in delays in loan releases. Banks may also impose various requirements which would pose difficulties for prospective borrowers, thus effectively discouraging loan availment.

- Using net disposable income as basis for computing the loanable amount for the loan ceiling levels above P150,000 will result in reduction of the amount that will be financed and, consequently, will compel the borrower to secure from other high-cost sources the difference between the loan granted and the price of the housing package attuned to his needs and actual capacity to pay.

- Limiting the function of origination only to banks will considerably reduce the volume of financing assistance. This would seriously impair the thrust of the National Shelter Program to service the largest number of underprivileged homeless families in the shortest time possible.

- The addition to the UHLP of a new window for market-oriented middle-income home financing simply duplicates the role that banks and financial institutions already play, even as it will compete for UHLP funds that – as originally intended – should be channeled in full to socialized and low-cost housing.

Albeit, it should be pointed out that even with this policy shift, the burden of collection remains with the NHMFC, considering that once the mortgages are already purchased from the banks, there is little assurance that the latter, without appropriate sanctions, will exert adequate effort as collecting agents.

It is likewise emphasized that the problem of enhancing NHMFC’s collection performance and, consequently, its cash flow, is basically an administrative matter that should be addressed through appropriate administrative and structural reforms, rather than through a policy shift that changes the entire complexion of the UHLP and only creates greater problems.

RECOMMENDATIONS

As a more effective alternative, CREBA reiterates its original recommendations concerning the UHLP and home mortgage financing in general, as follows:

1. Maintain the UHLP as originally conceived for socialized and low-cost housing, with the following features:

- Developers as originators under the CTS mechanism (Annex A). Adoption of the CTS mechanism as proposed by CREBA will eliminate any problem concerning the integrity of mortgages, and will fully insulate the NHMFC from risk in case of defaults by borrowers;

- Increased loan ceilings based on geographic categorization (Annex B);

- Reduced lending rates at 6%, 9% and 12%. The cross-subsidy feature of the UHLP under this lending rate structure will be achieved without impairing the NHMFC’s viability, once the low-cost fund sourcing schemes (Annex C) proposed by CREBA are put in place;

- Fixed investments of investible funds by SSS, GSIS and Pag-IBIG into the UHLP (in lieu of the current annually negotiated contributions) to be effected through the issuance of Special Housing Bonds (5-year term, at not more than 9% interest); and

- Option on the part of the borrower to secure credit insurance or to put up equity.

2. Establish the proposed Home lending Banks’ Network (HBN) to formally tie-up with the SMMS for purposes of home mortgage origination by banks and mortgage trading by NHMFC (Annex C).

CREBA’s recommendations did not prosper. However, its recommended housing finance reforms were included in the congressional bill for the creation of a Department of Housing and Urban Development, which CREBA had been advocating since 1994. (The bill was approved in 1997 by the Lower House under the leadership of Speaker Jose De Venecia; unfortunately, the Senate failed to act on the counterpart bill before the 1998 elections.)

In 1996, as the NHMFC was on the verge of insolvency, the Funders (SSS, GSIS & HDMF) completely refused to release their funding commitments and, under a Memorandum on Housing Finance between the Department of Finance, Department of Budget and Management, and the Funders, the processing and collection of mortgages was transferred from the NHMFC to Pag-IBIG. In effect, this move reverted the home financing back to its original institutional framework.

Thereafter, HUDCC issued Board Resolution No. 12 which dismantled the UHLP and replaced it with a program called Multi Window Lending System (MWLS).

CREBA lodged a formal protest against the MWLS, citing several flaws, the most serious of which was the allocation of a substantial portion of the funds for developmental loans, instead of using these funds exclusively for homebuyer financing.

A CREBA whitepaper provided a detailed analysis of the issues and proposed solutions. Again, CREBA’s protest did not prosper.

Under the Estrada Administration

By 1999, the NHMFC was insolvent, saddled as it was by “non-performing assets” resulting from failure to collect the mortgage receivables from the home loan borrowers. The secondary market remained underdeveloped; the National Shelter Program in 13 years managed to serve only some 300,000 out of the 4.5 million homeless families; the shelter industry was in a moribund state, with the mortgage takeout backlog reaching P7 Billion; and the socialized housing program was at a complete standstill.

CREBA then elevated its proposed shelter finance scheme – the Centralized Homebuyer Financing Program (CHFP) – together with a draft EO – to then President Joseph Estrada.

CREBA also called for the President to revoke HUDCC Resolution No. 12 and abolish the MWLS. The cover letter to the President said:

The program involves tapping some P120 Billion from purely private sources and completely do away with government budgetary outlays or subsidies, which the government simply cannot afford, and maintaining the socialized housing loan rate at 9%.

It may be instituted at any time by an Executive Order, without need of Congressional action, since it is anchored on existing laws.

As an urgent first step, there is need to (1) revoke the Ramos administration’s HUDCC Resolution No. 12 and the succeeding HUDCC Resolution of former Chairman Karina David, and (2) issue a Presidential directive to SSS, GSIS, Pag-IBIG and the Central Bank to operationalize the transfer of funds to NHMFC under appropriate arrangements.

Thereafter, CREBA’s proposed Shelter Finance Scheme may then be installed, to avail of the following benefits:

- It will facilitate realization of the administration’s pro-poor thrust, since the entire P120 Billion facility will be channeled exclusively to socialized and low-cost housing beneficiaries, at a 9% interest rate for a full credit term of 25-30 years.

- It will solve fund sourcing problems, and do away with government budgetary outlays for subsidies. The credit facility will revolve and depend entirely on private funds.

- Unlike previous schemes where funding came in trickles of only P5 to P10 billion annually, this Scheme will generate substantial funds that will enable production of some 400,000 units per year.

- Unlike previous programs which limited the credit facility only to members of SSS, GSIS and Pag-IBIG, under CREBA’s Scheme all underprivileged homeless families may avail of the credit facility even if they are non-members of these institutions.

- It is foolproof and impermeable to abuse by any vested interest. Corollarily, through the contract-to-sell (CTS) mechanism which involves developer guarantees on 100% collection, it will correct the flaw of previous NHMFC policies which resulted in poor loan collection performance.

- The concerns of all UHLP participants – i.e. the borrowers, funders, developers, banks, the government, and the investors under the proposed securitization program – have all been addressed, are fully protected, and will be equitably served.

- It is sustainable on a year-to-year basis through securitization.

- The scheme is not only equitable and just, but is perfectly tenable under the Constitution and existing laws such as EO 90, RA 7279, RA 8435 and the Charters of SSS, GSIS, Pag-IBIG and NHMFC.

- Unlike previous funding programs which were designed only to meet the production targets of the incumbent administrations, CREBA’s proposed program if instituted will transcend presidential tenure and serve as the Administration’s lasting legacy to the nation, to endure until homelessness is completely resolved in time.

The Battle

CREBA’s public information campaign for the CHFP and criticism of the MWLS incurred the ire of Leonora De Jesus, then HUDCC Chair and Estrada’s Presidential Adviser on Housing.

The HUDCC denigrated CREBA’s position with public pronouncements, maligning the CREBA leadership and citing housing production figures as proof of the success of the National Shelter Program. CREBA refuted the claims as being bloated.

This triggered a long-running, bitter media war between the HUDCC leadership and that of CREBA.

Failing to get the CREBA leadership to stand down, a divide-and-conquer strategy was adopted to get the CREBA membership to renounce affiliation and repudiate its leaders.

The stratagem backfired when, in an unprecedented show of unity, all but one of the presidents of CREBA’s chapters nationwide voluntarily trooped to Calamba, Laguna to adopt a resolution affirming support for the CREBA leadership.

The long-running conflict between HUDCC and CREBA escalated to the point that Congress called a hearing to provide a formal forum for the parties to shed light on the issues.

From the hearing, the Congressional Committee on Housing directed the HUDCC to revoke its Resolution No. 12 and dismantle the MWLS.

Succeeding Administrations

Under the administration of President Gloria Macapagal-Arroyo, CREBA continued to push for an Executive Oder to institute its proposed housing finance reform package under the CHFP, even as it continued to push for the creation of a Department of Housing.

In 2000, then Congressman Eduardo Zialcita filed a bill to enact an Omnibus Housing Act, containing CREBA’s recommendations for the creation of a Department of Housing, as well as its proposed measures for equitable land access and the shelter finance measures. However, Congress failed to act on this bill.

After the end of Arroyo’s presidential term and her election to Congress, among her first acts as a Representative was to file a bill to institute the CHFP.

To date, the bill is pending in Congress, having been refiled by Representatives Micaela Violago and Ferdinand Martin Romualdez.

As the country awaits, the number of low-income families without their own homes – now at 6.7 million – continues to rise.

CREBA’s quest continues.